워너 뮤직 그룹은 유니버설 뮤직 그룹, 소니 뮤직 엔터테인먼트와 함께 "빅3" 음반사 중 하나로 새로운 음악 콘텐츠의 유일한 상장 음반 회사이다. 워너 뮤직 그룹(WMG)은 주식 당 25달러에 상장된 이후 첫 번째 수익을 발표했다. 올해 다른 모든 기업공개(IPO)와 마찬가지로 초기에 시장의 주목을 받았지만, 워너 뮤직 그룹은 그 이후 하락세를 보였다.

스트리밍의 성장이 비즈니스의 다른 영역에서의 도전을 상쇄하지 못하면서 수익이 감소했다. 그러나 긍정적인 측면으로는 워너 뮤직 그룹이 비용 구조를 절감시키는 것은 물론 신흥 아티스트들의 큰 'sophomore' 히트곡을 달성했다.

Data by YCharts

그러나 올해 실적에 대한 반응은 엇갈렸다. 코로나 대유행의 영향으로 올해 워너 뮤직 그룹은 비틀거렸고 스트리밍 부문의 기록적인 결과에도 불구하고, 워너뮤직의 물리적 음악 판매는 훨씬 더 빠른 속도로 감소하고 있다.

워너 뮤직 그룹의 현재 시가총액 147억7000만 달러, 기업가치 171억7000만 달러(현금 55억3000만 달러, 가장 최근의 대차대조표 30억 달러)

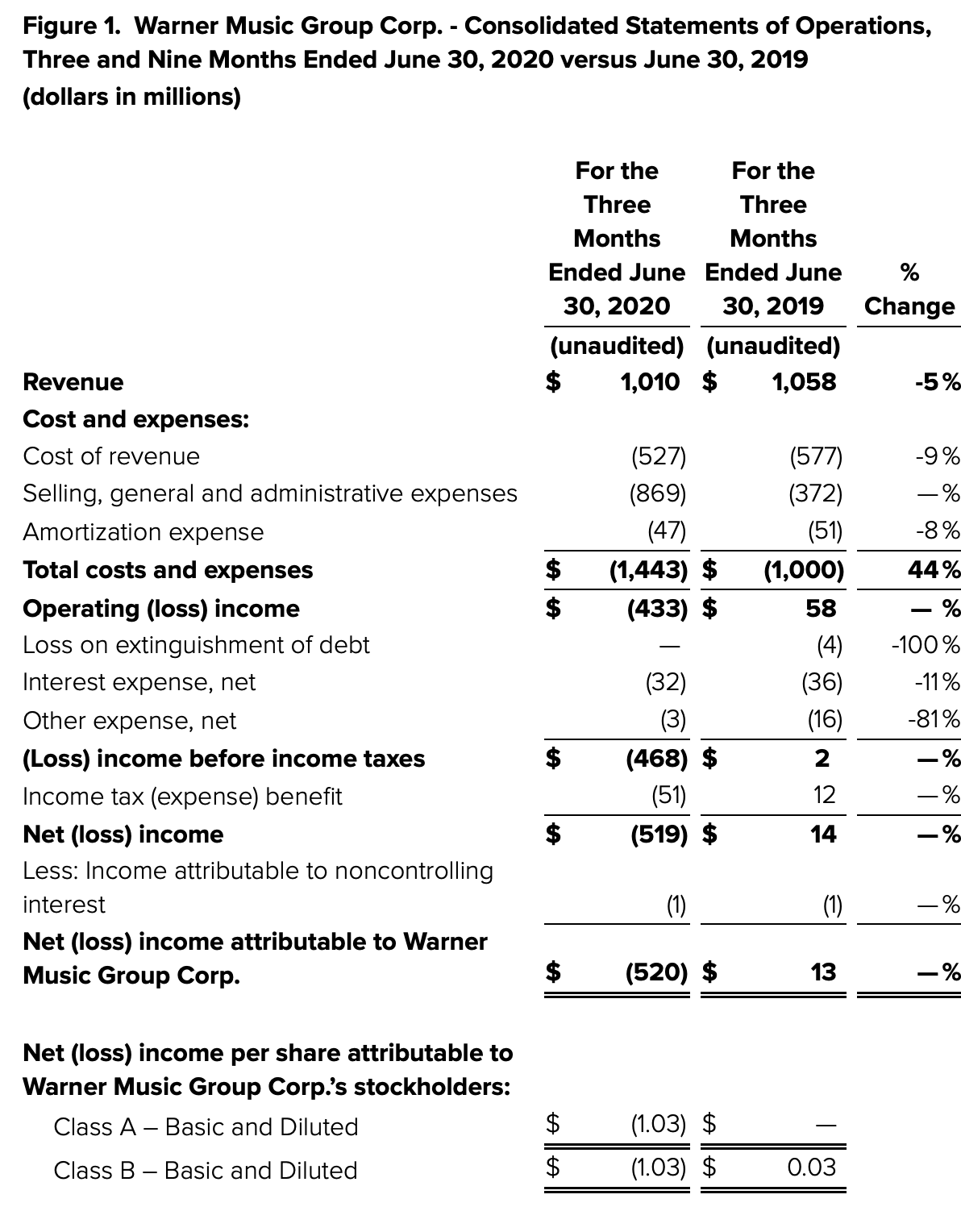

분기 수익 요약은 다음과 같다.

Figure 1. Warner Music Group Q3 results

Source: Warner Music Group Q3 earnings release

워너 뮤직 그룹의 수익은 -5% y/y를 기록하며 10억 1천만 달러로 줄어들었다.

이는 월스트리트의 기대치인 9억8천만달러(-7% y/y)를 2포인트 차로 앞섰지만, 20년 회계연도의 첫 두 달 동안 워너 뮤직 그룹이 기록한 y/y 매출 증가율 1.5%에는 미치지 못했으며, YY19년(또한 동사의 최고치인 OIBDA)에서 달성한 y/y 성장률 12%에는 크게 못 미쳤다.

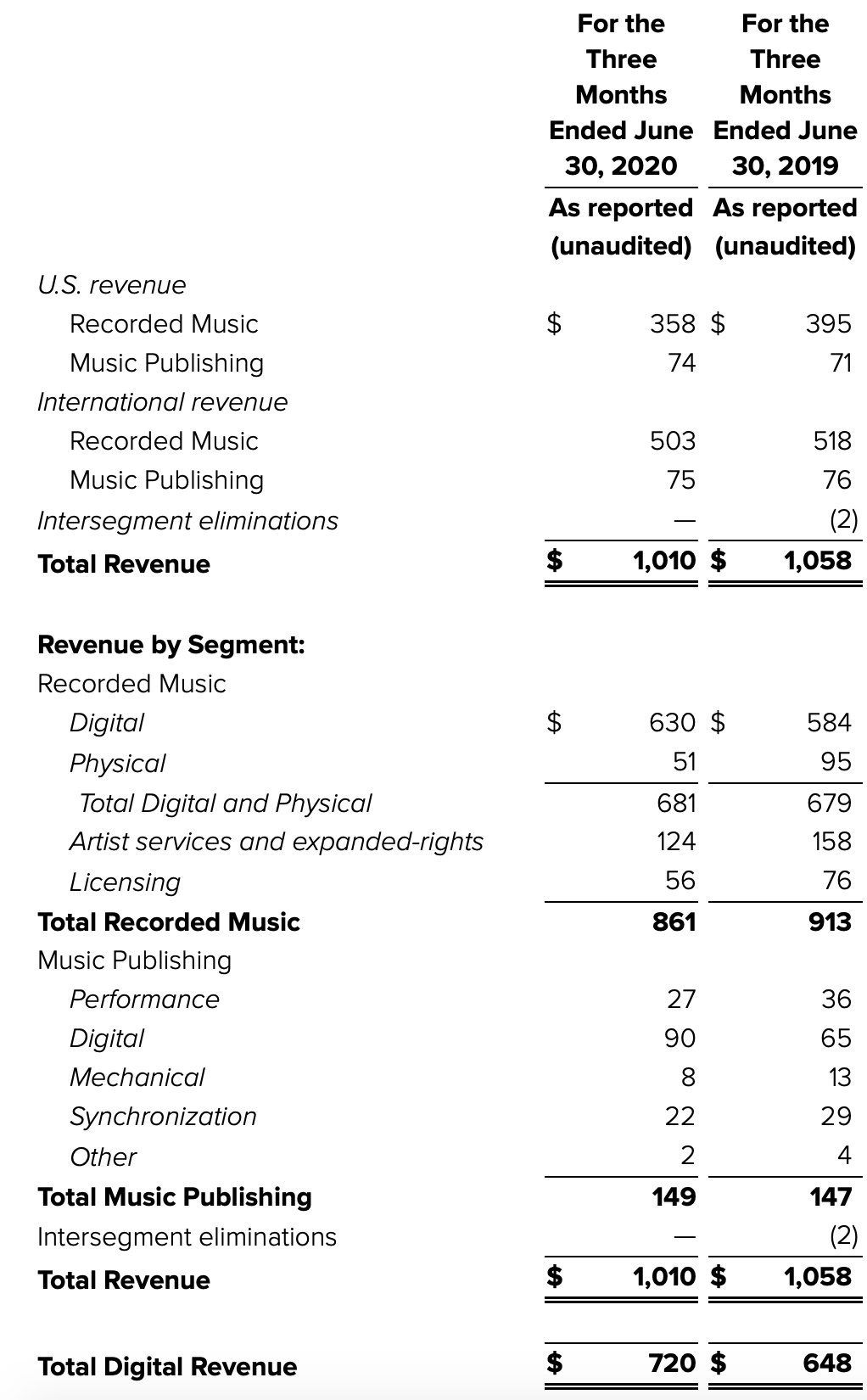

Figure 2. Warner Music Group revenue by segment

Source: Warner Music Group Q3 earnings release

The good news: as expected, due to the booming popularity of streaming services on which Warner Music Group earns a cut of royalties paid per stream, the company achieved 8% y/y growth in digital revenue. We note, however, that this is weaker than the 9% y/y pace in digital growth that Warner achieved in the first half of FY20. And in addition, while Warner Music Group previously was able to utilize growth in streaming to offset declines in its legacy businesses, the declines in physical music (-46% y/y) and artist services (-21% y/y) this time were too steep to overpower.

To some extent, some portion of Q3's revenue disappointment was directly attributable to the pandemic. Artist services revenue has declined because big promotional music tours as well as headlining festivals like Coachella have been cancelled or indefinitely postponed. Not only are these events direct revenue generators (through both tickets and merchandise), but they are also major opportunities to promote and market new music and new artists. On the bright side, we can expect these revenues to return once lockdowns ease and people feel comfortable in crowds again, and there may be an element of pent-up demand for music events once that happens.

Not all of the revenue shortfall, however, can be blamed directly due to the coronavirus. Physical music sales have been declining and cannibalized by streaming for years. The good news is that physical music is now a much smaller portion of the overall business, so by next year physical revenue won't cause as much of a drag on the y/y compares.

The good news

There are small pieces of silver lining within Warner Music Group's third-quarter results, however, that help to support the bullish cause for this stock.

The first is anecdotal, and it regards the company's propensity to produce new hit music. Similar to filmed entertainment companies, broad back libraries are still useful in driving sustained royalty revenues, but what keeps a studio alive and thriving is an ability to consistently produce strong new content.

Steve Cooper, Warner Music Group's CEO, noted that some of the biggest hits of Q3 were from newer "sophomore" artists within Warner's portfolio. Per his prepared remarks on the Q3 earnings call:

We’re especially proud of our ability to attract original talent often early in their careers and develop them into global superstars. Our commitment to new artist development is illustrated by the fact that 4 out of our top 5 best sellers this quarter were from artists releasing either debut or sophomore albums: Dua Lipa, Lil Uzi Vert, Roddy Ricch and Tones And I.

In the U.S., Nielsen’s 2020 midyear report again proved our ability to have massive hits with artists at every stage of their careers. This included Roddy Ricch’s hit single, The Box, which is the most streamed song of 2020 and the only track with 1 billion streams in the U.S. alone. We also had 3 of the top 10 artists by total consumption as well as the number 1 and number 2 biggest pop songs during the first half of the calendar year."

Success in new artist development means that Warner isn't going to be overly reliant on one or two big hits (a parallel example to illustrate this in the movie world is Lionsgate Entertainment - after the massive success of the four Hunger Games films which collectively grossed ~$3 billion worldwide, the company hit a multi-year revenue shortfall). What's more important than the individual hits is that Warner Music Group has the process, the know-how, and the organizational setup to keep producing strong content.

The second piece of good news is on the profitability front. Despite the decline in revenue, Warner Music Group was able to capitalize on a planned reduction in marketing expenses to drive improvements in OIBDA. On an adjusted basis, OIBDA actually grew 12% y/y to $166 million, representing a 16.4% adjusted OIBDA margin - up 240bps versus 14.0% in the year-ago quarter.

The last positive update is on Warner Music Group's capital structure. Right after the close of the third quarter, the company managed to refinance $535 million of its debt to take advantage of lower interest rates. Warner's CFO commented that the company was able to bring down its weighted average cost of debt from a rate of 4.0% to 3.6% post-refinance, saving $9 million in interest costs on an annual basis (or about 20bps of annual revenue). Yes, it's small, but in a lower-growth business like Warner Music Group where operations and execution are everything, every cost optimization counts.

Key takeaways

There are certainly positive highlights to note for Warner Music Group, and the fact that the company remains the only way to express a concentrated bet on music publishing/music content will continue to make it an interesting name to follow. Given the current valuation premium and revenue declines amid COVID-19, however, I wouldn't rush into buying the stock.

'금융' 카테고리의 다른 글

| [동남아시아 아마존] 씨그룹,Sea Limited(NYSE:SE) 강한 성장세와 위험요소들 (0) | 2020.10.19 |

|---|---|

| [알리바바,BABA] 두프리 면세점 지분 획득, 핀테크 강자 알리바바 분석 (0) | 2020.10.12 |

| 플러그파워 Andy Marsh CEO 인터뷰 기록(20.08.08.) (0) | 2020.09.19 |

| 유럽의 버크셔해서웨이, 내스퍼스(네스퍼스,프로수스,PROSY) (0) | 2020.09.17 |

| [SQUARE,SQ,ARKF] 스퀘어, 핀테크 시장과 함께 성장중 (0) | 2020.09.16 |

{kind=link}

{kind=link}

댓글